How Resilient?

By Bas van Geffen, senior macro strategist at Rabobank

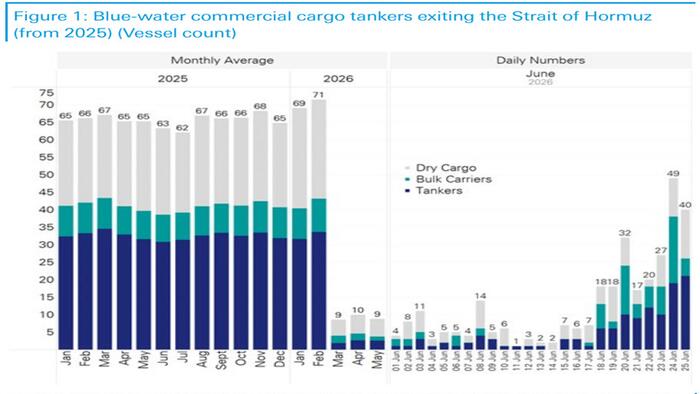

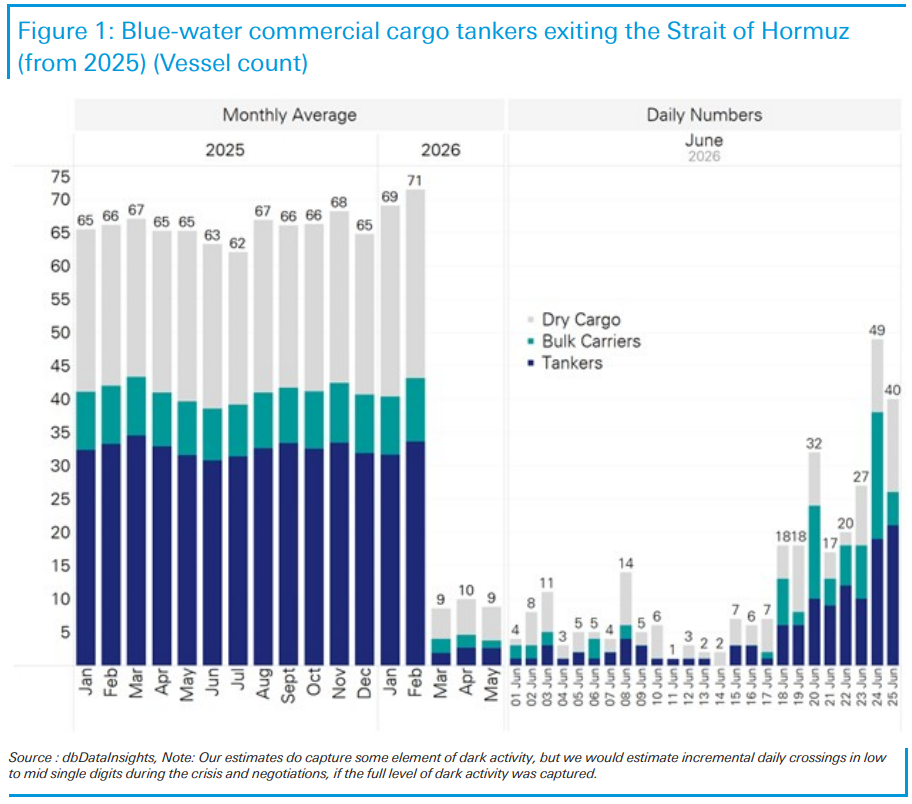

A cargo ship was hit by an unknown object near the coast of Oman yesterday. The vessel took some damage, but the company reported that “crew, vessel, and cargo are all safe.”

The ship has since left the strait, and tankers continue to transit. Still, these attacks force a rethink about the safety of the Strait of Hormuz, just as shipping from the Gulf region was starting to pick up again. The International Maritime Organization temporarily halted its evacuation plan for ships leaving the Gulf, and several tankers changed course – possibly after instructions from Iran.

US officials stated the ship had been struck by an Iranian drone. And one of these officials said the hit was likely deliberate: the drone had manoeuvred to the side of the ship before it attacked. Plus, the incident happened just hours after the IRGC had warned ships to only use the routes that Iran had approved. Vessels that do not are “not covered by the safe passage guarantee.”

That could of course be coincidence. However, if Iran was indeed behind the attack, the IRGC warning was perhaps not out of concerns that there might still be mines in those shipping lanes, but because there aren’t. That is, perhaps, ships were exiting at a faster rate than Iran had foreseen, as it tries to retain as much leverage as possible during the talks with the US. Or maybe Iran was unhappy that Oman cooperated with the US and the UN, by allowing vessels to transit through its side of the strait.

The attacks are the latest in a series of tests whether the memorandum of understanding will be upheld by both sides. The Israeli incursion into Lebanon is another. Iran has said that Israel must leave Lebanon today, but Prime Minister Netanyahu has no intention to withdraw.

However, energy markets seem to believe the deal will hold. At $73.8 for a barrel of Brent, crude prices are still towards the lower end of this week’s trading range, despite the latest incident in Hormuz.

Indeed, as fragile as the deal may be, both Iran and the US have a motive to stick to it – even though US officials blamed Iran for the incident, they also immediately downplayed the incident. The MOU allows Iran to sell oil and Iran may be able to get some resources back into the hurting economy. Meanwhile, President Trump admitted that US “economic catastrophe” loomed within four to six weeks, if the MOU had not been signed and the stalemate had continued.

So, earlier this week, we updated our scenarios. We now expect talks to continue – possibly for longer than the 60 days that were originally agreed to in the MOU. However, ultimately the set of outcomes is limited to Iran or the US getting the better deal, or new tensions if neither side is willing to accept defeat. We assume the latter outcome as our base case failing a shift in Iranian deliverables on tolls, uranium, and Hezbollah. However, it is a close call and the timing is near-impossible to predict.

Whilst not of “catastrophic” proportions yet, the Iran war is clearly starting to show in US economic data. US PCE inflation rose to 4.1% in May, in line with expectations. Underlying inflation has been accelerating since late last year, and that trend was kept intact.

Core inflation came in at 3.4%, which is the fastest pace in 2.5 years’ time. In the Powell-era, this used to be the Fed’s favourite inflation indicator. Warsh’s favourite metric gives the Fed a little more respite, perhaps. The trimmed-mean PCE inflation rate, ticked up to 2.4%, a level it has been hovering around since the turn of the year. But the key driver behind accelerating core inflation were services prices, notably in financial services, insurance, and transportation services. Pressure from tariff hikes has continued to build gradually as well. So, overall, stickiness seems to have broadened somewhat.

Despite these higher prices, US consumers continue to spend. Real personal spending increased by 0.3% m/m, which was a little better than expected – however that does come on the back of a slight downward revision of the April data.

Another potential risk to consumer spending is the shifting sentiment about AI and tech stocks. Fresh doubts about the AI rally left the Kospi index 7% lower on the week, after a rollercoaster ride that triggered circuit breakers on the way down. The mood soured on Tuesday and Wednesday. Then, Micron’s bumper earnings report reassured investors somewhat. But tech stocks are leading the decline again today.

The Korean index indicates growing caution about AI and tech. That is not limited to the Korean index, but global markets are still more composed. European equities are broadly opening in the red – albeit much less dramatically than the Kospi’s 5.8% loss on the day, or the 4.2% decline in the Japanese Nikkei.

These doubts about the sector are despite -or because of?- European plans to become digitally sovereign. Earlier this month, the European Commission adopted a “tech sovereignty package.” And the EU joined the US’ Pax Silica this week, which excludes China from supply chains for AI-capable semiconductors.

The agreement is a non-binding declaration of intent. Nonetheless, it will certainly anger China. The declaration follows on earlier discussions on trade imbalances, which the EU now sees as a more urgent problem. The Commission is looking to implement a law that requires EU companies to diversify their supply chains, which is mainly aimed at de-risking from China – even though Brussels did not name the country specifically. Beijing has already said it would retaliate.

And blocking China from AI supply chains is insufficient. If the European Commission is serious about tech sovereignty, then it must also be prepared to pick a fight with the US over its role in European technology – or at least accept that subsequent steps towards autonomy could lead to retaliatory measures from Washington.

More pressing, perhaps, are the trade tensions surrounding the renewal of the USMCA, the free-trade agreement between the US, Mexico and Canada. Although the agreement does not expire on 1 July, it does face its first mandatory six-year joint review. The FT reports that the car industry could derail the agreement – or may at least put a strain on negotiations.

The US has effectively banned Chinese cars, and the US automobile industry will pressure President Trump to uphold that ban. However, Canada and particularly Mexico have embraced Chinese cars. The Canadian minister of Industry has recently met with Chinese carmakers to explore investments in Canadian production capacity. That may be incompatible with US policy, and review of the USMCA. At the same time, any new trade deal may become a bit less attractive to Canada if Chinese investments make the Canadian auto industry less dependent on the traditional North American supply chain.

Related Markets

All MarketsMarket data may be delayed. Not financial advice.

💡 AI analysis provides alternative perspectives on current events

{kind=link}