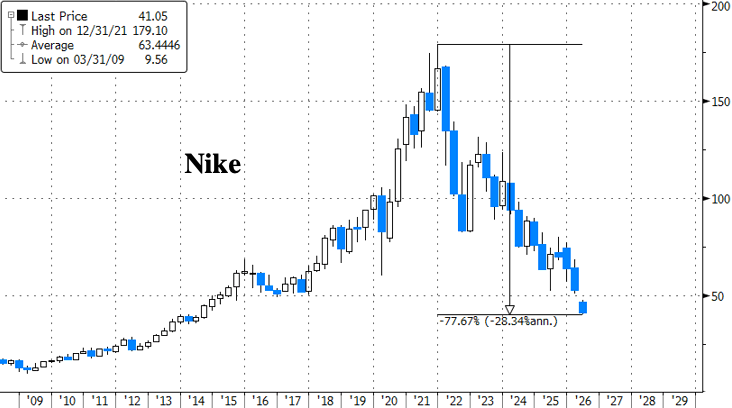

Nike Turnaround Falters As UBS Says There's "No Reason To Buy" Stock

Nike shares fell 3% in premarket trading after the struggling athletic apparel giant warned on its earnings call that revenue declines over the next two quarters will be worse than previously expected, underscoring that there is still no immediate turnaround to halt a multi-year bear market that has driven the stock to decade lows.

"We are not expecting the environment to improve meaningfully over the next six months," Nike's outgoing CFO Matt Friend told investors on Tuesday evening.

Customers are "under pressure around the world, and we can particularly see it having a larger impact on sportswear," Friend added.

Nike now sees sales falling in the low-to-mid single digits, down from an earlier view of a low-single-digit decline. The slowdown is expected over the next six months and is mostly due to slower wholesale shipments in North America, among other factors.

The downbeat commentary offset better-than-expected fourth-quarter sales and profits, which were largely in line with expectations. Management warned that the operating environment became "increasingly challenging" as the quarter progressed, with North America slowing by mid-April.

Our immediate takeaway is that Nike's reset remains ongoing, and any turnaround plan will likely take much longer than initially anticipated, continuing to pressure the stock.

UBS equity analyst Jay Sole, focused on retail, department stores, specialty softlines, apparel, footwear, and consumer discretionary stocks, was blunt with clients: "We don't see a reason to buy the stock."

Sole explained why clients should hold off for now from attempting to bottom-fish the stock, which is currently trading at 2014 levels:

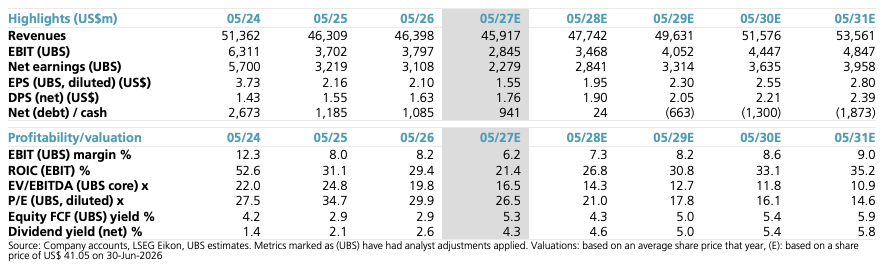

The pivotal Nike question remains "Is all the 'bad news' now priced in?" Despite the pullback in Nike's stock price, we still don't see a good entry point. Nike's stock price is still not cheap at ~27x our FY27 EPS estimate, in our view, and this suggests a solid rebound remains priced in. We continue to see a balanced upside/downside skew. The main upside risk is Nike returns to positive sales growth with expanding gross margin faster than expected. Yet the main downside risk is the rebound takes much longer than the market anticipates. Nike's 4Q report did not cause us to change our thesis much.

Nike's 4Q report underscores upside and downside sales and margin risks:

1. Nike lowered its CY26 sales guidance, but there were bright spots within the outlook. Nike lowered its CY26 sales growth forecast to -L to -MSD% from -LSD %. We believe the main negative factor is Nike's fashion business continues to struggle. The issue is Nike's fashion business remains 50% of its sales mix. Nike may need to take this percentage much lower over time in order to reestablish itself at the world's best sports brand. If so, it could serve as a major, multiyear drag on Nike's top line. This is the main downside sales risk. At the same time, Nike's performance business grew 5% in Q4. Plus, the company sounded like it is in the process of replicating the operational improvements made in categories like running to other sports categories such as basketball, training, outdoor, and tennis. If so, this could lead to upside sales growth surprises over the NTM. This is the main upside risk, in our view.

2. Nike offset its lowered sales expectation with raised margin guidance. Nike boosted its GM% outlook slightly and trimmed its SG&A outlook in order to maintain its CY26 guidance. This was a mild positive surprise to us and Nike is citing its ability to continue to tightly manage costs as one means of restoring its EBIT margin back to 10% over time. However, Nike's average annual SG&A growth rate over the past 4 years (FY27e included) is just 0%. Our concern is Nike is underinvesting in future growth in order to limit near-term downward EPS revisions. Thus, a main downside margin risk is that Nike will have to ramp up SG&A more than expected to return to sustainable top-line growth.

We maintain our FY27, FY28, and FY29 EPS estimates:

We lower our FY27 sales growth forecast given Nike's plan to reduce its inventory buys. Plus, we see greater revenue pressure post Q1 as Nike moves past major sporting events like the world cup and laps elevated promotions on its digital channel. At the same time, we raise our operating margin forecast related to annualizing new efficiencies in Nike's supply chain and technology divisions. Plus we see slightly lower risk Nike's promotions

Separate analyst commentary (courtsey of Bloomberg):

Bloomberg Intelligence analyst Poonam Goyal

- "Nike's sales recovery is likely to take longer as management tightens buys and sell-in to clear sportswear, Jordan, streetwear and China inventory, even as margin can expand sooner"

Citi analyst (neutral, PT to $45 from $47)

- Nike's sales are looking a little weaker, while margins are a little better.

- “After sales slowed in mid-April within 4Q26, June (1QTD) has improved, helped by excitement around global football"

Guggenheim analyst Simeon Siegel (buy, PT $60 from $74)

- The bottom line is that "we assume investors will still question whether Nike has 'ripped the band-aid' on earnings revisions"

- Trim price target on "recognizing ongoing noise and a general reduction in retail multiples"

Jefferies analyst Randal Konik (buy, PT to $75 from $90)

- The fourth-quarter report "came in ahead with kernels of progress solidifying in the base business"

- "Sportswear/Jordan Streetwear still the overhang, but not getting worse"

RBC Capital analyst Piral Dadhania (sector perform, PT $50)

- Revenues remain reliant on wholesale, whilst direct-to- consumer trends remain soft, which is "not likely sustainable mid-term"

- "Nike has delivered a mixed 4Q26 quarter (ex US tariff refund) with anticipated lack of underlying revenue momentum offset by more favourable FX translation benefit which flatters absolute gross profit"

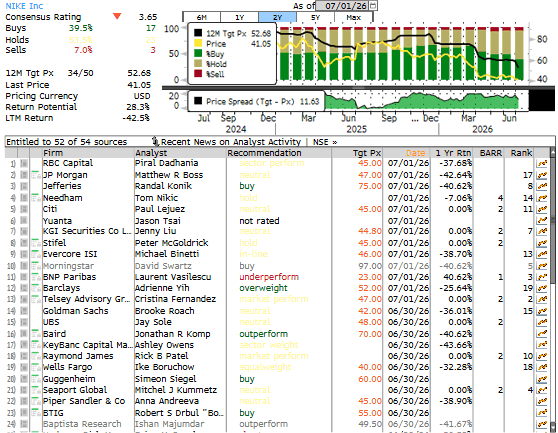

According to Bloomberg data, there are 17 "Buy" ratings on the stock, with 23 "Neutral" ratings and 3 "Sell" ratings.

Read The Market Ear note on Nike's epic demise titled "Go Woke Go Broke: Nike Stopped Obsessing Over Athletes And Started Obsessing Over Activism."

Related Markets

All MarketsMarket data may be delayed. Not financial advice.

💡 AI analysis provides alternative perspectives on current events

{kind=link}

{kind=link}

{kind=link}

{kind=link}