"Results Were Tempered": Pepsi Blames US Snack Slump On Cash-Strapped Consumers

PepsiCo blamed the second-quarter slowdown in its North American food unit on consumers tightening their belts. The period was marked by elevated pump prices tied to the US-Iran war, a squeeze that hit lower-income households the hardest and weighed on discretionary snack and beverage purchases.

Revenue in the company's North American food unit fell 2%, while volumes remained flat, even as the junk food giant slashed prices on some of its brands by as much as 15% earlier this year to lure working-class consumers.

"Results were tempered in the quarter as U.S. food and beverage category performance moderated with consumer budgets tightening due to rising inflationary pressures," CEO Ramon Laguarta stated in a press release.

"Our North America business was softer than we anticipated in the second quarter, and we now expect a more gradual improvement in performance trends for the balance of this year," CFO Steve Schmitt said in prepared remarks.

PepsiCo reaffirmed its full-year guidance and reported adjusted earnings of $2.20 a share for the second quarter, slightly above the Bloomberg Consensus estimate.

The company has also raised prices on some smaller bags and is expanding its product line to include more protein and fiber as consumer tastes shift toward healthier options.

Here's JPMorgan analyst Andrea Teixeira's first take on PepsiCo earnings:

The earnings beat was of lower quality, driven mostly by below-the-line items and OSG came in a tick below expectations as North America underperformance was offset by stronger International. PFNA turned negative again after a strong start in 1Q26, with volumes decelerating to flat vs. +2% in 1Q, as management noted that U.S. food and beverage category performance moderated in the second quarter amid higher inflationary pressures. Management reiterated guidance (in line with our expectations and preview), but is now expecting a more gradual improvement in trends in North America and is now embedding a ~1 point benefit to EPS from tariff refunds in the guidance (mostly occurring in 3Q and allocated to PBNA, with the company likely to use these tariff refunds to offset higher COGS and reinvest in A&M to reignite volumes). The company is also pointing to 4Q-weighted EPS growth in 2H. PEP turnaround is deep and investors should not expect a straight line as with most restructurings in CPGs, yet we think investors will need to get more reassurance in consumption data ahead in order to feel more confident that the ingredient reformulation, brand restaging and affordability actions are working.

Peter Grom of UBS' first take:

Initial Reaction: Negative. Heading into the print, given weaker tracked trends in North America our conversations suggested most anticipated organic sales to be under pressure with much of the debate centering on how company frames the full year outlook and the path from here. Against that backdrop, we think the print more or less played out as expected but was still disappointing on the surface relative to consensus as organic sales fell short, GM/ OPM came in below with total company EPS ahead of expectations due to favorable below-the-line items. From a guidance perspective, the company maintained their outlook and while they did not point to the low end of the range (as some expected), management did outline that growth is expected to be 4Q weighted. While this is not surprising on the surface given the external environment and timing of input cost pressures, we would note that simply hitting the low end of the range implies +HSD EPS growth in 4Q against a tougher comparison on the bottom line - which some are likely to view as optimistic. In many ways we do not think the print will be viewed as thesis changing and although it would not entirely surprise us to see shares trade higher today given positioning, based on the quality of the print/outlook alone, we would expect shares to trade lower this morning (currently -1.2% pre-market).

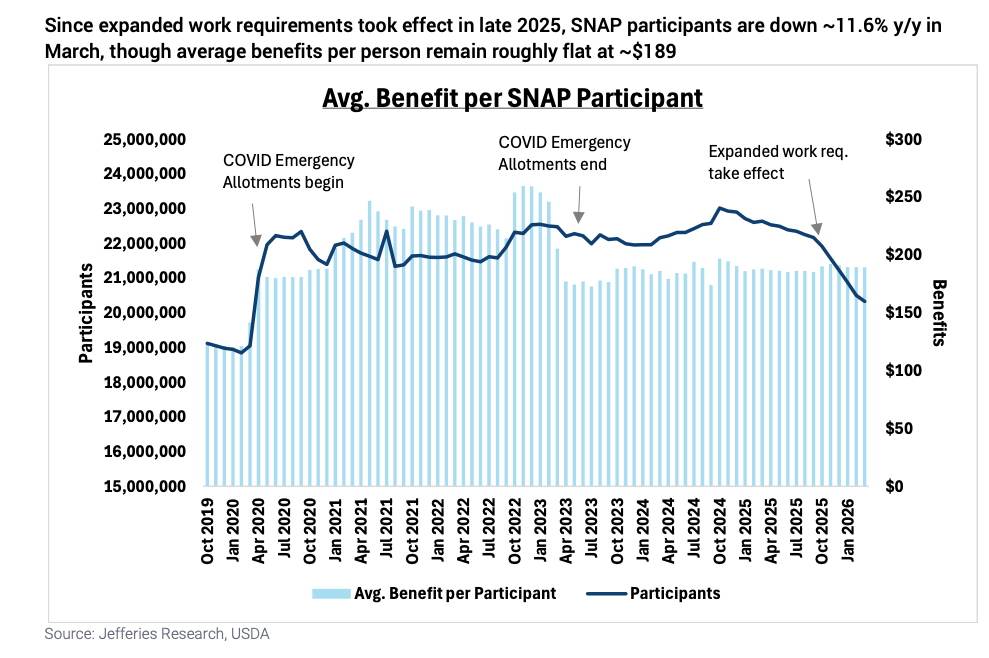

Separate but notable is a chart from food retail equity analyst Scott Marks at Jefferies that shows a sharp decline in average benefits per SNAP participant (read report) ...

Pepsi shares slipped nearly 2% in premarket trading Thursday. The stock is down about 1% year-to-date and lagging the broader S&P 500 index.

Related Markets

All MarketsMarket data may be delayed. Not financial advice.

💡 AI analysis provides alternative perspectives on current events

{kind=link}

{kind=link}