JPMorgan Drops Despite Highest Quarterly Profit In HIstory, As Traders Focus On Negatives

Q2 earnings season is officially off.

Moments ago, JPMorgan became the first mega bank to report Q2 earnings (technically Wells beat it by a few second but nobody really cares about that particular bank), firing the starting pistol on the second quarter earnings season. The Q2 results were solid (Net Interest Income and FICC miss but more than offset by blowout Equity Sales and Trading and Investment Banking revenue) , but as we note in out bank earnings preview last night, perfection (and beyond) was already largely priced into the stock which has become a true hedge fund hotel, and as a result the stock is modestly in premarket trading.

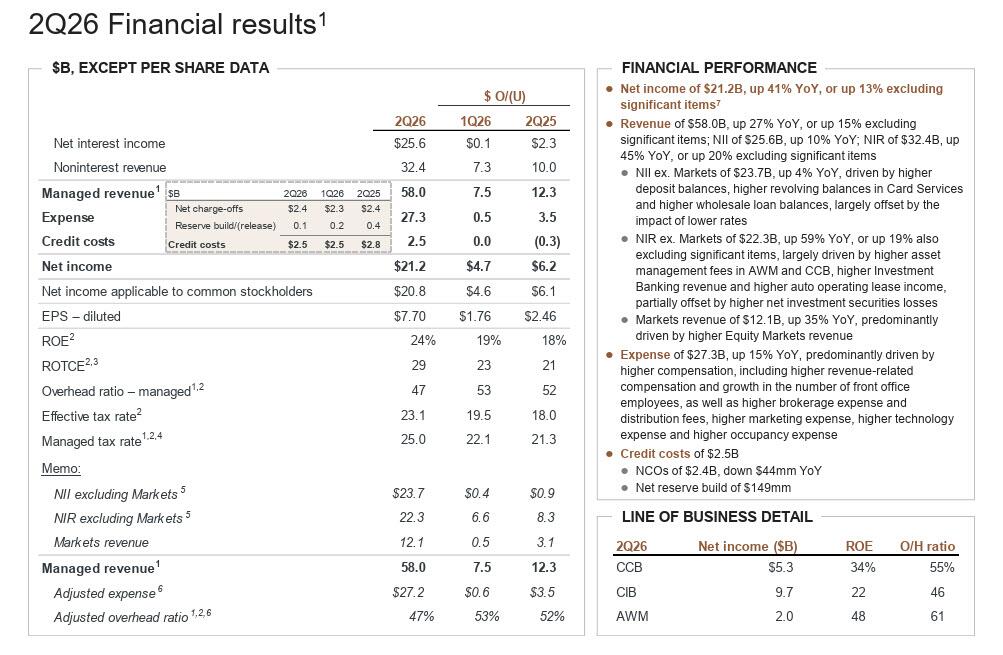

Here is a snapshot of what the company reported for Q2:

- EPS $7.70, beating est. of $5.58, and up $2.46 YoY

- Revenue:

- Adjusted revenue $58.02 billion, smashing est $51.39 billion, and up $12.3 billion YoY

- Managed net interest income $25.62 billion, missing est, $25.64 billion

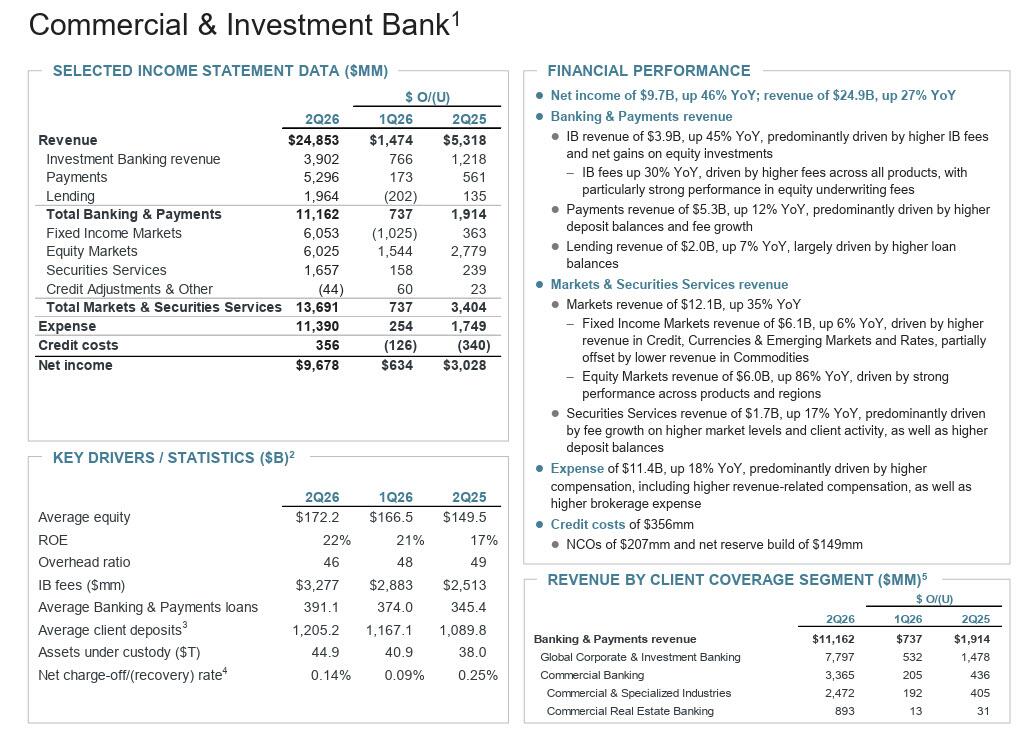

- Total Commercial and Investment Bank revenue $24.85BN, up $5.32BN YoY

- FICC sales & trading revenue $6.05 billion, missing est. $6.29 billion with weakness in commodities

- Equities sales & trading revenue $6.03 billion, smashing est. $3.98 billion

- Investment banking revenue $3.90 billion, smashing est. $3.06 billion

- Advisory revenue $1.01 billion, missing est. $1.07 billion

- Equity underwriting rev. $829 million, beating est. $621.3 million

- Debt underwriting rev. $1.44 billion, beating est. $1.17 billion

Let's take a closer look at JPM's Q2 earnings.

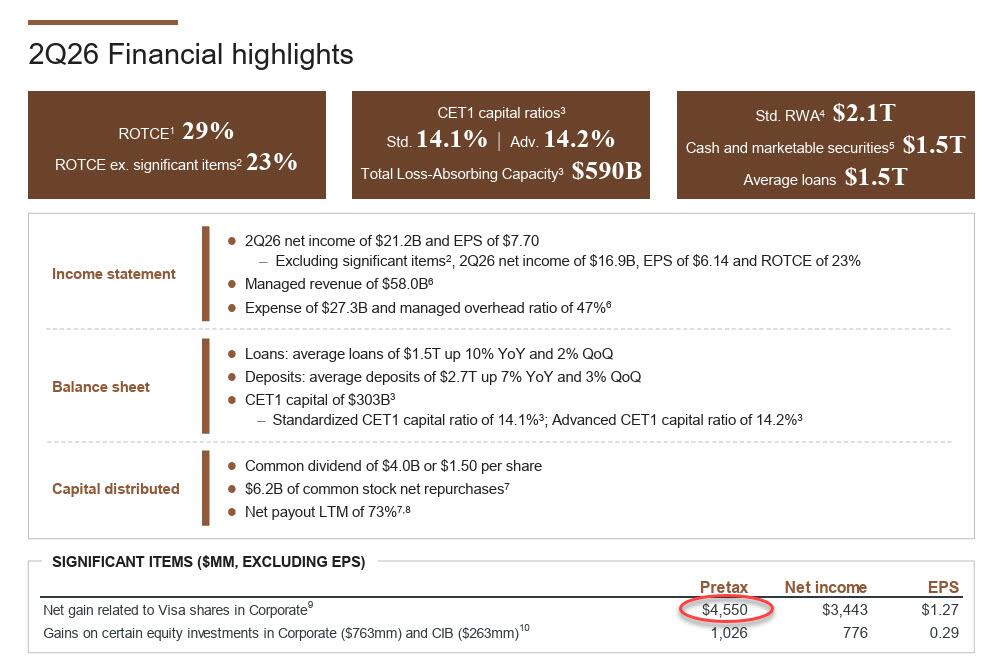

First, the good news: JPM reported its highest quarterly profit ever as stock traders blew past analysts’ estimates and a long-held Visa stake paid off to the tune of $4.6 billion. Indeed, a notable one-off item that contributed to the firm’s success this quarter was JPMorgan' $4.6 billion net gain related to the sale of Visa shares. The bank said this in its earnings supplement: "The net gain was “related to Visa Class C common stock held at fair value and received by the Firm in an exchange offer following the acceptance by Visa Inc. on May 11, 2026 of the Firm’s tender of its 18.6 million shares of Visa Class B-2 common stock.”

More good news: equity trading was stellar, with Q2 equities revenue rising 86% from a year earlier to $6.03 billion, anmd more than $2 billion higher than expected; In fact, it beat even the highest estimate among analysts surveyed by Bloomberg and brought total trading revenue to $12.1 billion, more than the previous all-time high set in the first three months of this year.

There was bad news: FICC revenue of $6.05 billion missed estimates of $6.29 billion with weakness in commodities Additionally, while Investment Banking beat, advisory revenue of $1.01 billion missed estimates of $1.07 billion. And while managed net interest income increased by more than 9% from a year prior to $25.62 billion from $23.31 billion last year, it was a slight miss to the $25.64 billion estimate.

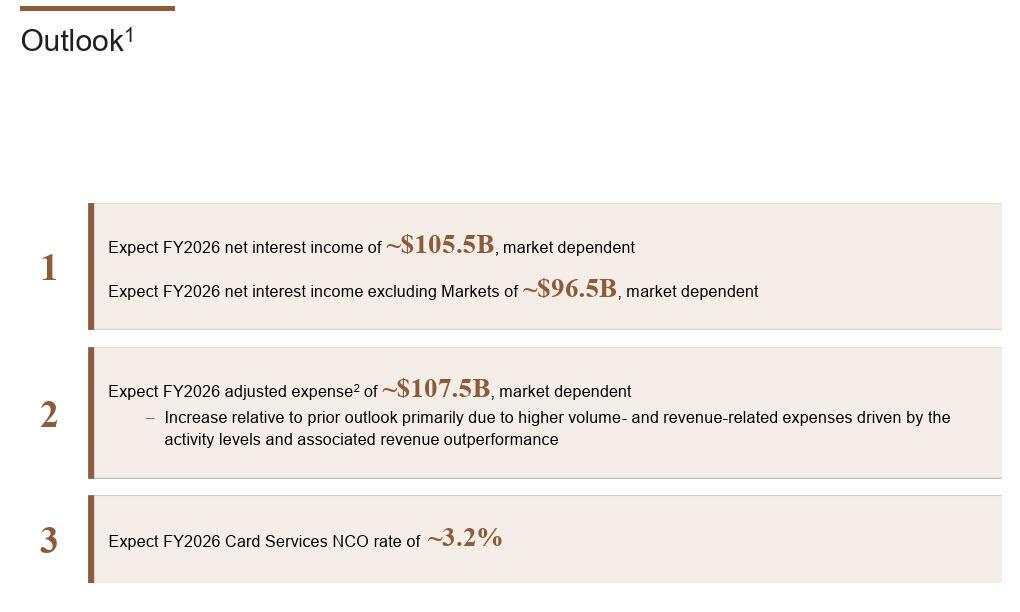

There was some more bad news, this time on the expense side: Q2 expenses were $27.3 billion, more than expected. The firm also updated its full-year cost guidance to about $107.5 billion, beyond the increase Dimon telegraphed at an industry conference in May.

Investment banking was in focus in the wake of SpaceX’s record initial public offering in June. JPMorgan pulled in $3.28 billion in investment-banking fees in the second quarter, beating estimates and up 30% from a year earlier "driven by higher fees across all products, with particularly strong performance in equity underwriting fees."

The bank’s provision for credit losses – how much JPMorgan expects to lose from uncollectible loans – was $2.52 billion for the period, significantly less than the $3.09 billion that analysts had expected. Of this, net charge-offs were $2.37 billion, also below the estimate $2.62 billion.

Even as almost every business exceeded expectations, CEO Jamie Dimon was cautious about prospects for the future.

“Several risks are shifting below the surface like tectonic plates, including geopolitical tensions and wars, sticky inflation, large global fiscal deficits and elevated asset prices,” Dimon said in the statement. “We cannot predict how these forces will ultimately play out. They may remain manageable, but they could also cause meaningful disruptions when they shift or collide.”

Jamie Dimon also pointed out that card annual fees jumped by more than 30%, “reflecting healthy retention levels after recent product refreshes as well as demand for our premium products.”

Looking ahead, the firm expects full-year net interest income to now be about $105.5 billion, after previously anticipating it would be around $103 billion. For the quarter, it came in at $25.5 billion. That, however, comes along with the increase in full year expenses to $107.5BN. In a presentation Tuesday, the firm said the increase is “primarily due to higher volume- and revenue-related expenses driven by the activity levels and associated revenue outperformance.” For the quarter, expenses were $27.3 billion, more than expected.

The bank also said it expects the full-year net charge-off rate in its credit-card business to come in at around 3.2%, lower than the 3.4% guidance it provided in April.

The report comes as Jamie Dimon is finally preparing his sucession: last month, the bank named Troy Rohrbaugh and Doug Petno co-presidents of the firm, the latest twist in the race to succeed Dimon, 70, when he eventually steps down. The bank said longtime executive Marianne Lake would retire as part of the changes, with Rohrbaugh replacing her atop the company’s sprawling consumer arm and Petno gaining sole control of the commercial and investment bank.

Looking back, today’s report isn’t helping the priced to perfection stock, which has been a laggard year-to-date on a total-return basis -- up only about 5% including dividends through yesterday. Morgan Stanley, Goldman Sachs and Citigroup all delivered more than 20% including payouts, and Bank of America has returned more than 9% by that measure. Wells Fargo is the standout loser, down almost 5% this year even after counting dividends.

Shares of JPMorgan, up 3.8% this year through Monday, fell 2.6% in early New York trading.

Full Q2 invest presentation below (pdf link)

Related Markets

All MarketsMarket data may be delayed. Not financial advice.

💡 AI analysis provides alternative perspectives on current events

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}