Private Credit: The New Junk Bond Market

Authored by Ed Dowd via Beyond the Narrative,

Private Credit: The New Junk Bond Market...Except It Lacks Transparency, Liquidity & Is About To Be Stress Tested

History

Private credit was born from the ashes of the Great Financial Crisis. In the aftermath of that debacle, regulators moved to limit the risks banks could take. Loans deemed too risky were no longer being originated by commercial banks. To fill that void, non-bank lenders stepped in, creating what is known as private debt or direct lending market. You may know these vehicles as Private credit funds, also referred to as business development companies (BDCs). These funds raised capital from pensions, endowments, insurance companies, and wealthy individuals.

Unlike junk bonds or corporate bonds, these loans are not publicly traded and are typically held to maturity. In fact Private credit has quietly taken a big chunk of market share from the traditional junk bond market. These private deals give borrowers speed, confidentiality, and customized terms they can't always get from public bonds, while investors get higher yields and perceived lower volatility. The public junk bond market has actually improved in average credit quality as the riskier companies moved into these opaque structures.

The funds have traditionally targeted middle-market companies with revenues between $10 million and $1 billion, though the strategy has recently expanded to larger firms and bigger deals, including those in AI. Last November Morgan Stanley estimated that of the $1.5 trillion in external financing needs for the projected AI datacenter buildout that as much as 50% could be funded by Private credit (hold that thought).

One notable drawback of private credit funds is their high degree of opacity also called a lack of transparency. These funds disclose limited information about their loans and mark their own books, which can potentially mask deterioration in the portfolio. Because of the illiquid nature of these assets and the lack of a public trading market, the investments are inherently illiquid and often include gating provisions should too many investors want their money back at the same time.

Growth

The industry started the way any small new industry does: by filling a niche need. The fee structure, while lower than that of private equity, remained extremely attractive to managers, with total effective fees often running from 3% to 4% of NAV. The pitch to investors was straightforward: higher yields than public bonds and lower reported volatility because there is no daily mark-to-market. The risks, of course, are illiquidity and higher default rates in a recession (hold that thought).

Bottom line: The fat fee structure attracted many firms to get into this business and the Wall Street sales machine was engaged, went into action and the money flowed into these firms.

The Last Two Years of Growth

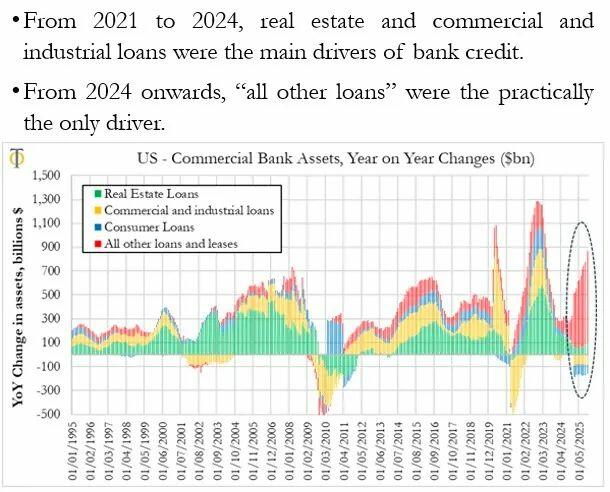

The industry itself is not nefarious, but like all credit markets, it is prone to excesses at the end of a cycle. Growth in assets under management (AUM) over the last two years (2024 & 2025) has been estimated at 50% to 75%. The entire category is now estimated to stand between $2.5 trillion and $3 trillion in AUM. When you examine credit creation across the broader banking system over that same period, most of the incremental loan growth in the economy flowed to these non-bank institutions from commercial banks (See chart below).

The key question investors should ask is: With this explosive growth in AUM and competition for loans in the industry, have the funds found enough creditworthy borrowers in an already high-risk category, or rather did the inflows chase incrementally "junkier" credits with looser loan covenants?

Trouble in Paradise

Starting in the fourth quarter of last year, several high-profile Private credit bankruptcies emerged, most notably First Brands and Tri-Color Auto. Questions about the structure of Private credit funds began to surface, particularly around opacity and illiquidity. This led to investor redemptions and the gating of several prominent funds in Q1, including those from BlackRock, Blackstone, Apollo, Cliffwater, Blue Owl, and others. The pressure continued into Q2, with redemption requests accelerating across these major platforms. The problem is not improving, rather it is getting worse.

Implications

Effectively, the Private credit markets are now shut down and at best stalled. They are in redemption mode which could ultimately lead to liquidation mode at subpar pricing. While some new loans may still be originated, the market as a whole has slowed dramatically. As noted previously, we saw that the marginal credit creation of the past two years in the US economy has come from an industry known for being opaque and illiquid...and that driver of credit is now in question. The critical questions are: how large are the losses, how long will this downturn in private credit last, and what will recovery rates look like? PIMCO (one of the largest fixed income investors) has recently stated that the credit default cycle has begun and that losses will be higher than expected, with clear implications for the broader economy.

To make matters worse the lack of transparency and public quotes make determining what is going on in these funds extremely difficult for the capital markets to assess other than the fact that we are seeing outflows from the sector. The investors have unanswered questions and are like mushrooms growing in the dark on manure.

Private credit woes may also have implications for the commercial banking system. I mentioned above that most of the credit creation from commercial banks in 2024 & 2025 was Private credit and Private equity. Private credit funds rely on bank credit lines (subscription lines, NAV facilities, revolvers) for liquidity and leverage. These have grown rapidly with contingent liquidity to Non-Depositary Financial Institutions (NDFIs) standing at approximately $2.3 trillion overall, with Private credit market share rising over the last few years. Simultaneous drawdowns from credit stress in Private credit could transmit shocks to bank balance sheets. I don't believe it's a systemic problem yet but it bears watching. At a minimum it would likely curtail commercial bank enthusiasm for overall credit creation in the economy (i.e. consumer loans, commercial & industrial loans and real estate loans).

Earlier I told you to hold two thoughts in your head. First that AI funding datacenter buildout was contingent on the Private credit market to fund 50% of the external financing, and secondly, the default rates in Private credit would be higher in a recession as advertised initially by the industry. Given that flows in the Private credit industry are going the wrong way, and the industry is effectively paused...I don't see how AI data center build out will be funded by Private credit in the near term, and secondly I believe the industry's recession default assumptions are about to be tested very soon and could be higher than expectations.

Conclusion

Credit is the lifeblood of economic activity, and recently a great deal of it has flowed through this new channel. Significant losses have yet to be fully recognized, and they will ultimately hit pension funds, insurers, asset managers, and wealthy individuals who hold these investments. The commercial banks also have exposure to this market and losses in this sector could lead to a broader credit contraction. And finally, AI financing could become prohibitively expensive and pause or dramatically slow the capital expenditure cycle, affecting what has now become about 45% of the S&P 500's market capitalization.

I believe the feedback loops are already underway and are likely to spread to the economy and eventually the equity markets.

P.S. If you are interested in a much deeper nitty gritty dive into Private credit markets and the risks check out the Unicus Investor on Substack: The Unicus Investor - Blackstone's BCRED: Earned $0.54. Paid $0.60. Cut to $0.54.

Disclosure: I have no financial relationship with Unicus...I just think they do good work.

"Be careful that you do not forget the Lord your God... Otherwise, when you eat and are satisfied, when you build fine houses and settle in them, and when your herds and flocks grow large and your silver and gold increase and all you have is multiplied, then your heart will become proud and you will forget the Lord your God..." Deuteronomy 8:11-14

Related Markets

All MarketsMarket data may be delayed. Not financial advice.

💡 AI analysis provides alternative perspectives on current events

{kind=link}

{kind=link}