Europe's Utility Sector Is 'On The Brink Of A New Regime'

Authored by Gregor Morris via BondVigilantes.com,

Europe’s utilities sector is on the brink of a generational shift. After more than a decade of subdued demand, the system is being forced to modernize, rebuild and expand. Electrification, datacentres, renewable integration and ageing infrastructure are converging into what can only be described as unprecedented capital expenditure programmes across the sector.

Simplistically, the bullish narrative is a convergence of rising electricity demand, visible investment pipelines, increase in regulated investments and improving returns. However, the same forces driving growth are also set to reshape balance sheets, funding needs, and elevate execution risk.

A step change in capital intensity

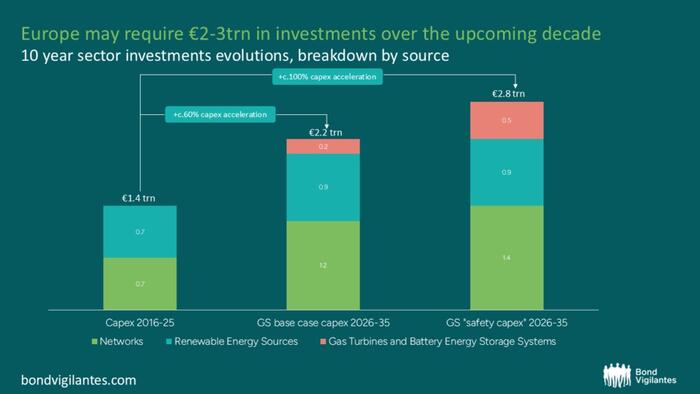

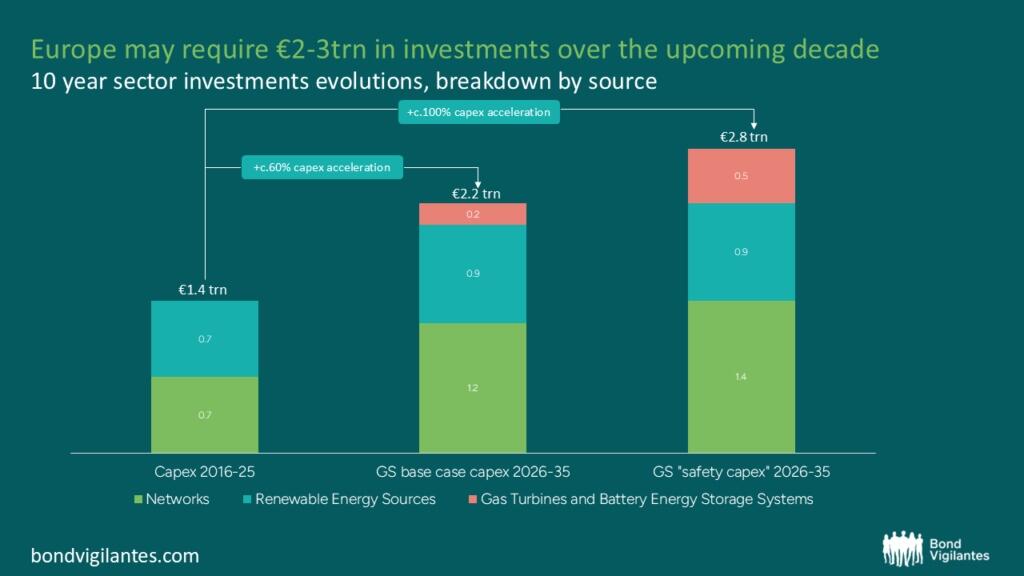

The scale of investment required is extraordinary and though we have seen some large equity cheques, the vast majority of investment need will be funded by debt issuance. The European power system is expected to require €2–3 trillion of capex between 2026 and 2035, up to double the previous decade’s spend.

According to Goldman Sachs, within this:

- €1.2–1.4 trillion is needed in power grids alone.

- Significant incremental spend is required for backup gas capacity (~€200bn) and battery storage (~€35bn by 2030).

Even over the next five years, the numbers are large: around €580bn of sector capex between 2026–30. With roughly 85% allocated to regulated or contracted activities, this does provide bondholders elevated security. On paper, capex visibility is high and earnings should be supported by regulated returns (particularly for grid operators) and contracted revenues (renewables). However, for credit investors, the issue is not just visibility of returns, but the timing mismatch between spending, cash flow generation, and regulatory recovery.

Source: Goldman Sachs Global Investment Research

Is leverage pressure structural?

Historically, utilities have been able to fund investment cycles with a mix of operating cash flow, disposals, and incremental debt while maintaining broadly stable credit metrics. This cycle looks materially different. As it stands, rating agencies have remain largely comfortable with declining FFO to net debt and rising debt burdens.

However, there are some marked differences. First is the sheer intensity of the capital increase. Second, the societal and political impact of increased pressure on the affordability of bills (across all utilities). Finally, the mis-match between up front capex and delayed cash flow realisation is worthy of note. Spending is upfront, whilst returns are earned over the long term, leaving balance sheets under pressure in the interim, even if returns are ultimately attractive.

For bondholders, this raises three key questions:

- Can we get comfortable with the amount of debt required to fund the capex?

- How quickly can companies recycle capital, through asset sales, project financing or partnerships?

- And the most important of all, are we being paid to take this risk?

Execution risk becomes a credit driver

In previous cycles, utility credit risk was heavily linked to commodity exposure or regulatory outcomes. In this capexcycle, execution risk is emerging as a primary credit variable.

The complexity of what needs to be delivered is unprecedented. Europe must simultaneously: retire old assets, build out renewables at scale (with generation increasingly weather-dependent), expand and modernise grids that are decades old and integrate new demand sources such as datacentres.

Each of these is challenging in isolation. Delivering them simultaneously introduces coordination risk across supply chains, permitting, and system planning. From a credit perspective, this matters because execution slippage directly translates into:

- Cost overruns → higher debt funding needs?

- Project delays → deferred cash flows and weaker coverage ratios?

- Regulatory lag → slower recovery of invested capital?

In other words, even if returns are contractually or regulatorily supported, cash flow timing becomes uncertain. For credit investors there could be some bumps along the way.

Related Markets

All MarketsMarket data may be delayed. Not financial advice.

💡 AI analysis provides alternative perspectives on current events

{kind=link}