The Six Vectors Of Gold Remonetization Revealed

Authored by Ronnie Stoeferle via VonGreyerz.gold,

A look at monetary history reveals that the question of “sound money” was never purely academic in nature but has always been of central importance for economic stability and social order. The past five decades of the pure fiat experiment are, measured against 5,000 years of monetary history, a brief anomaly. And anomalies tend to be corrected.

Our thesis of a remonetization of gold may seem bold at first glance, which makes a clear conceptual framework all the more important. Those waiting for the reintroduction of a classical gold standard will be disappointed: Governments have no incentive to voluntarily relinquish the fiscal and monetary flexibility that the fiat regime offers them. Rather, what is meant is a process in which gold regains monetary relevance. Not necessarily as money in the strict sense, but certainly as the ultimate reference asset for value, trust, and settlement.

This remonetization does not occur by decree, but through function; not through revolution, but through evolution; not a sudden fanfare, but a steadily rising crescendo. Paradigm shifts often creep in through customs, certainties, and economic necessities. Gold is not moving to the center of the system. Rather, driven by fiscal exhaustion, geopolitical fragmentation, and dwindling institutional trust, the system is moving toward gold.

What connects the following six vectors is a shared underlying structure: At each of these junctures, gold regains a key role as a store of value and a safe haven. Not all vectors will become reality simultaneously or in their entirety, but several parallel channels should suffice to sustainably strengthen gold’s monetary relevance.

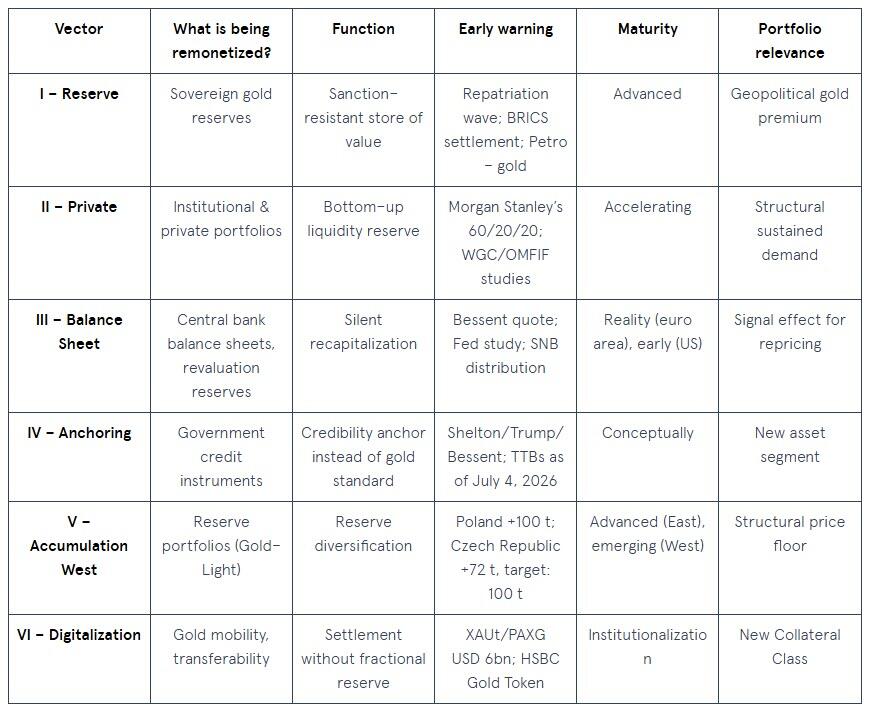

The six vectors

Vector I: Reserve Function & Sovereignty

Ever since the freezing of Russian reserves in 2022, it has become clear to many market participants that fiat reserves carry not only market risk but also political risk. Gold is the only major reserve asset without issuer risk. Repatriations in Germany, Poland, the Netherlands, and most recently France underscore this trend.

Vector II: Private Remonetization

Not only governments but also institutions are rediscovering gold as a store of value. Pension funds, family offices, insurance companies, and sovereign wealth funds have often held only minimal gold allocations to date. Even small shifts away from the global bond market could trigger enormous demand. Gold is thus evolving from a tactical allocation to a strategic liquidity reserve, from a “satellite” to a “core” investment.

Vector III: Accounting & Recapitalization

Gold functions not only as a reserve but also as an accounting lever. Since 1999, the Eurosystem has regularly valued gold at market prices; the resulting revaluation reserves effectively act as equity. In the US, too, the debate over revaluing gold reserves is gaining traction. In highly indebted countries, gold can thus become an instrument of silent recapitalization.

Vector IV: Anchoring Through Gold-Backed Bonds

Gold-backed government bonds could strengthen confidence and lower financing costs. Proposals such as those by Judy Shelton show that what is at stake is not a new gold standard, but a credibility standard. The difference between an unsecured government bond and a gold-backed one is similar to that between a promise and a pledge.

Vector V: Western Central Banks as Buyers

The major gold buyers in recent years have come primarily from emerging markets. The next phase could begin if Western central banks with low gold holdings—such as Canada, Japan, Australia, or the United Kingdom—replenish their gold reserves. Even moderate target reserves would generate demand equivalent to one year’s worth of mine production.

Vector VI: Digitalization

Tokenization could solve gold’s historical transaction problem. Gold-backed tokens combine physical scarcity with digital transferability. This positions gold as a competitor to fiat payment systems and CBDCs. The key factor remains whether ownership rights, backing, verifiability, and insolvency resilience are robustly structured.

The vectors described do not operate in isolation. A rising gold price improves central bank balance sheets, facilitates policy reassessments, strengthens the appeal of gold-backed bonds, and increases interest in tokenized forms of gold. It is precisely these feedback loops that make remonetization not a single event, but a self-reinforcing process.

Remonetization is taking shape

We are by no means the only analysts pointing to the possible evolution of the monetary system. Zoltan Pozsar had already elevated the debate on a new world monetary order to a new level in 2022 with his article “Bretton Woods III,” against the backdrop of sanctions on Russian currency reserves. He concluded his remarks with the following forecast: “From the Bretton Woods era backed by gold bullion, to Bretton Woods II backed by inside money (Treasuries with unhedgeable confiscation risks), to Bretton Woods III backed by outside money (gold bullion and other commodities).”

There is no question in our minds that we are irrevocably on a journey toward a new global (monetary) order. It will require an internationally recognized anchor of confidence. For several reasons, gold appears to be predestined for this role:

-

Gold is neutral – it knows neither flag nor ideology and is thus free from geopolitical manipulation.

-

Gold has no counterparty risk – unlike any claim or digital account entry, it exists independently, without relying on the promise of a third party.

-

Gold is liquid – with a daily trading volume of around USD 330bn, it ranks among the world’s most liquid assets.

-

Gold cannot be multiplied at will – gold reserves have been growing steadily by around 1.8% per year for decades. This geologically determined supply discipline is the fundamental difference from any fiat currency.

The composition of global currency reserves shows how far remonetization has already progressed. For decades, US Treasury bonds formed the backbone of official portfolios. Since the global financial crisis, the trend has reversed: The share of US bonds held by foreign central banks is declining, while gold is gaining significantly again. Despite significant purchases, emerging markets still hold considerably less gold than Western institutions.

What Connects the Six Vectors: Feedback Loops

As different as these six vectors may seem, they share a common underlying structure. In every case, gold regains monetary significance precisely where the existing system relies on trust, the quality of collateral, or political neutrality. Gold is not becoming more relevant because it has been modernized. It is becoming more relevant because the weaknesses of the alternatives are becoming apparent.

Feedback instead of addition

The key point is that the vectors do not act in isolation but reinforce one another. The cycle reads like a self-reinforcing engine:

-

Accumulation (Vector V) and private demand (Vector II) drive the gold price.

-

A rising gold price improves central banks’ balance sheets (Vector III).

-

Improved balance sheets reduce political resistance to gold-backed bonds (Vector IV).

-

Gold-backed bonds legitimize gold as a reserve asset (Vector I).

-

A higher, legitimized gold price makes tokenized gold products more attractive (Vector VI).

-

Tokenization, in turn, increases demand – and closes the loop.

This positive feedback loop is the actual catalyst. Once a critical mass is reached, the process accelerates on its own. Remonetization is thus not a binary event but a gradual phase transition. It can begin with reserves, gain traction through private portfolios, become politically relevant through balance sheet logic, and open up new areas of application through technological innovations. Those waiting for one big bang will overlook the crucial point: Systemic turning points are not heralded by decrees but by changing practices.

An Overview of the Vectors

Arguments against the concept – and why we remain convinced

However, there are also factors that argue against the remonetization of gold. The following structural objections deserve serious consideration:

-

The cash flow argument: Gold generates no current income. As long as government bonds are considered risk-free, the institutional incentive remains limited. Counterargument: It is precisely this status that is eroding – see Vector III.

-

The systemic risk argument: An erratic rise in the price of gold would destabilize the debt-based monetary system. Political resistance to this stems not from a conspiracy but from rational politics of interest. Counterargument: An orderly process like the Eurosystem model is in any case more attractive to policymakers than market chaos – the question is not if uncontrolled, but when controlled.

-

The substitution argument: Gold could lose its collateral function to other assets, such as Bitcoin or tokenized commodities. Counterargument: Complementarity is more likely than substitution (see the Bitcoin discussion in Vector III).

What would have to happen for the remonetization thesis to fail? Three scenarios are conceivable:

-

Significant debt reduction through real economic growth or fiscal consolidation

-

Substantial geopolitical détente with the lifting of all sanctions and a return to multilateral cooperation

-

A technological breakthrough in CBDCs that renders gold obsolete as an anchor of trust

Each of these scenarios is possible on its own. However, it is extremely unlikely that they would occur in combination. Remonetization would fail only if several secular trends were to reverse simultaneously.

The burden of proof has shifted

The real flaw in the current debate lies in what is considered normal. Over half a century of fiat regimes has clouded historical memory: The unbacked paper money system is now regarded as the norm, while gold is seen as a relic. Historically speaking, it is exactly the opposite. The past 54 years are the anomaly, and 5,000 years of monetary history are the proper frame of reference.

The burden of proof, therefore, does not lie with those who consider a gradual remonetization plausible. It lies with those who claim that a historically unique fiat regime will be able to function permanently without resorting to monetary anchors.

Back to the monetary future – this is also the title of the 20th-anniversary edition of the In Gold We Trust report 2026. It is not a nostalgic throwback. It is the sober realization that the history of money is longer and more cyclical than a single political cycle. Gold is not returning because it romanticizes the present. It is returning because the present can no longer keep its promises.

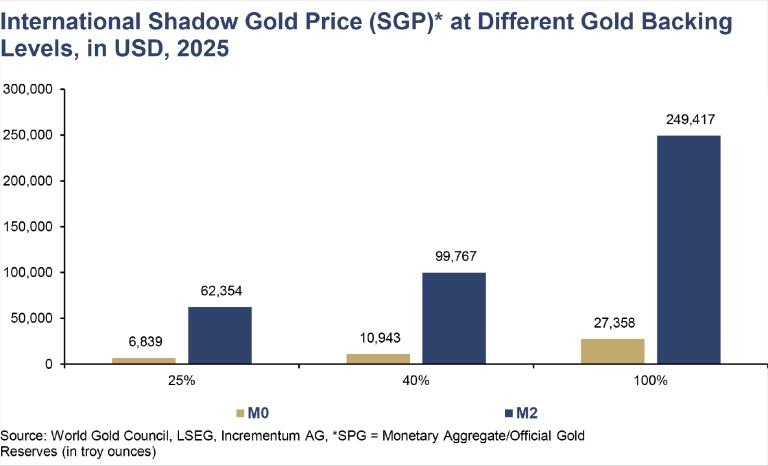

The shadow gold price

Should gold return to the center of the monetary system, the question of price consequences inevitably arises. An exact valuation is, by nature, impossible, but analytical approximations at least give us an idea of possible orders of magnitude. The best-known concept is the so-called shadow gold price.

The shadow gold price refers to the theoretical gold price at which the base money supply would be fully backed by gold. In other words: The shadow gold price is the price level at which a return to a fully backed gold currency would be mathematically possible. We do not consider such 100% backing of M0, as is sometimes advocated, to be necessary; it would currently imply a gold price of USD 20,900 per ounce. During the era of the gold standard, the market forced central banks to maintain coverage ratios between one-third and one-half, which corresponds to a current gold price between USD 7,000 and USD 10,400 per ounce.

Let’s take it a step further and look at the global level. The international shadow gold price corresponds to the gold price that would result if the central bank gold reserves were to cover the money supplies of the leading currency areas – the US, the euro area, the UK, Switzerland, Japan, and China – weighted by their share of GDP. The result reveals the extent of monetary expansion: With 100% coverage of the broad money supply M2, the gold price would be just under USD 250,000; even at a moderate 25%, it would be over USD 60,000.

Related Markets

All MarketsMarket data may be delayed. Not financial advice.

💡 AI analysis provides alternative perspectives on current events

{kind=link}

{kind=link}

{kind=link}