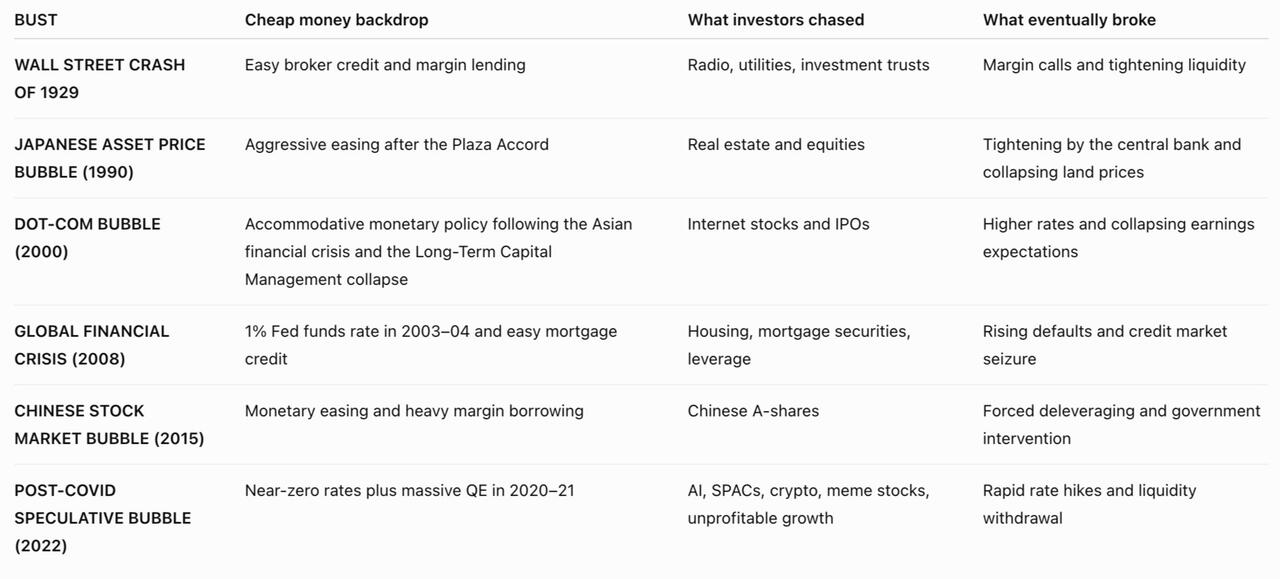

Your Delusion Doesn't Make Me A "Doomer"

Submitted by QTR's Fringe Finance

"There exists in society a very special class of persons that I have always referred to as the Believers. These are folks who have chosen to accept a certain religion, philosophy, theory, idea or notion and cling to that belief regardless of any evidence that might, for anyone else, bring it into doubt. They are the ones who encourage and support the fanatics and the frauds of any given age. No amount of evidence, no matter how strong, will bring them any enlightenment. They are the sheep who beg to be fleeced and butchered, and who will battle fiercely to preserve their right to be victimized."

- James Randi

One thing I’ve noticed over the last several weeks is that the more I stick to basic questions, basic economics, and basic skepticism, the more people accuse me of being a “doomer”.

That tells me far more about the environment we’re in than it does about myself. The foundation to my economic views hasn’t changed all that much over the years. What’s changed is the backdrop against which those views are being expressed. When you’re living through one of the most euphoric investing environments in modern history, ordinary skepticism suddenly reads like blistering, outright nihilism.

Apparently it’s now considered bearish extremism to point out that a company says one thing and then does another. It’s “FUD” to ask whether a proposed $2 trillion IPO valuation for a company trading roughly 100x sales while remaining unprofitable makes any sense. It’s negativity to observe that the Federal Reserve appears trapped between an inflationary rock and a deflationary hard place, where fighting one problem inevitably worsens the other. I’ve even written about companies that appear to have been caught engaging in outright misleading accounting practices that deserve far more scrutiny than they’re getting, only to watch investors shrug and buy more shares anyway.

None of the above observations strike me as outrageous. They’re the kinds of questions investors used to ask before narratives became more important than numbers. The fact that simply asking those questions now provokes outrage tells me something has changed.

Yesterday I nearly lost a dear longtime friend who I respect immensely because he was upset that I criticized Strategy CEO Phong Le on Twitter. The worst part is this is a friend who I agree with on literally almost everything relating to markets and monetary policy…just not on cheerleading for bitcoin as enthusiastically.

I can’t take Strategy or its CEO seriously after the company repeatedly emphasized BTC Yield as one of the defining metrics of the business. It was presented as evidence of execution, discipline, and shareholder value creation. Phong Le talked about it constantly. It became one of the pillars supporting the entire investment story for Strategy. Then, as the number began moving in the wrong direction, the company quietly stopped highlighting it. It disappeared from Michael Saylor’s tweets talking about how much bitcoin the company bought last month. And somehow I’m the unreasonable one for noticing this and calling it out as moving the goalposts (more importantly, I called my friend and we hashed it out and are fine).

Over the last several weeks I’ve also lost multiple paid subscribers to my blog. Some comments have become more cagey. Private messages have become more emotional. Discussions that used to revolve around facts increasingly revolve around motives. Apparently asking for consistency and follow through from public company CEOs now qualifies as “hate.” Ironically, I appreciate every bit of it because I don’t want an echo chamber. Echo chambers make people intellectually lazy. If everyone agreed with everything I wrote, I’d probably stop challenging my own assumptions. I like hearing opposing viewpoints. I’ve changed my mind plenty of times over twenty five years in markets. What I’m trying to arrive at isn’t confirmation. It’s truth. That distinction matters.

Part of the reason I view markets differently is because my framework has always been grounded in Austrian economics. Whether you agree with the Austrian School or not, one thing it relentlessly emphasizes is that incentives matter, prices matter, capital allocation matters, and economic reality eventually matters. Artificially suppressing interest rates has consequences. Printing money isn’t free. Debt doesn’t magically disappear because politicians or central bankers wish it away. Malinvestment accumulates. Capital gets allocated to projects that never would have survived under honest market conditions. Booms fueled by cheap money eventually collide with reality. Those aren’t particularly radical ideas. In fact, for most of economic history they would have been considered fairly obvious observations.

The Austrian framework forces you to ask uncomfortable questions all the time. Is this asset actually worth what people are paying for it, or has liquidity overwhelmed price discovery? Is this company creating durable cash flows, or simply issuing securities into an insatiable market? Are executives maximizing shareholder value, or exploiting shareholder enthusiasm? Are prices reflecting genuine economic value, or simply reflecting trillions of dollars in monetary distortion? Those questions naturally make you skeptical, not because you’re pessimistic, but because skepticism is the rational response whenever incentives become distorted.

That puts me in a very different place than many investors today, and I don’t say that to sound superior. I’ve simply been around long enough to remember markets before zero interest rates became totally normal, before quantitative easing became permanent policy and before passive indexing vacuumed up trillions of dollars regardless of valuation. Before gamma squeezes, meme stocks, perpetual options speculation, and social media turned investing into something that often resembles a casino more than capital allocation. Many people investing today have literally never experienced a market operating without extraordinary monetary accommodation.

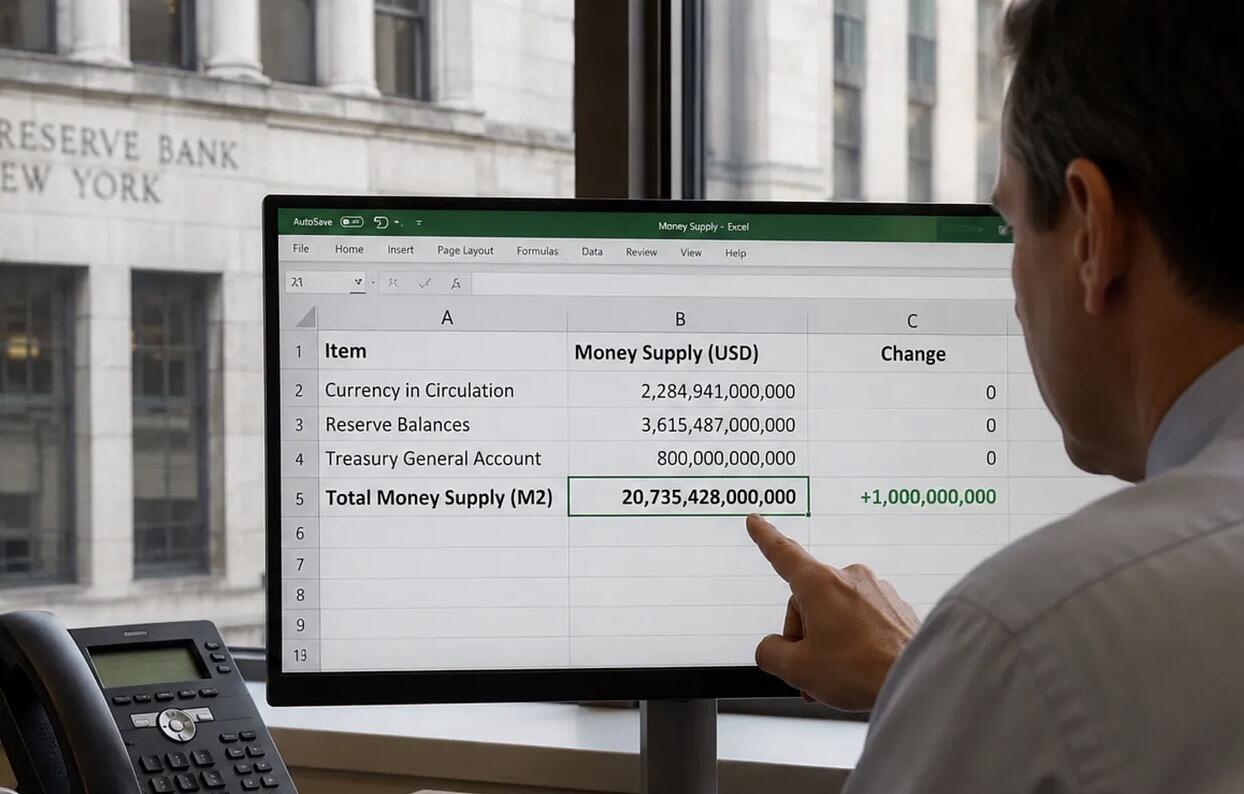

If you’ve only invested during an era where every crisis is met with another liquidity program, another balance sheet expansion, another alphabet soup lending facility, and another trillion dollars created electronically, your expectations become calibrated around that environment. Eventually you stop recognizing the distortion because the distortion becomes normal. When markets become uncalibrated, investors become uncalibrated too. When asset prices become detached from economic reality for long enough, people begin confusing price appreciation with proof of correctness. We used to have to come up with gold to put more money in circulation. Then, after that, we used to have to at least print actual dollars. Now, we increase the money supply by literally just moving f*cking commas on an Excel spreadsheet somewhere at the New York Fed office. It’s as easy as how I’m typing these words right now: Boom. Another trillion.

People start believing valuation no longer matters because it hasn’t mattered recently. They assume management credibility is irrelevant because stocks keep going up anyway. They conclude accounting quality doesn’t matter because nobody gets punished. They believe debt doesn’t matter because refinancing has always been available. They mistake liquidity for genius. They mistake speculation for investing. They mistake momentum for truth. None of this is really an indictment of individual investors. It’s what decades of monetary distortion do to human psychology.

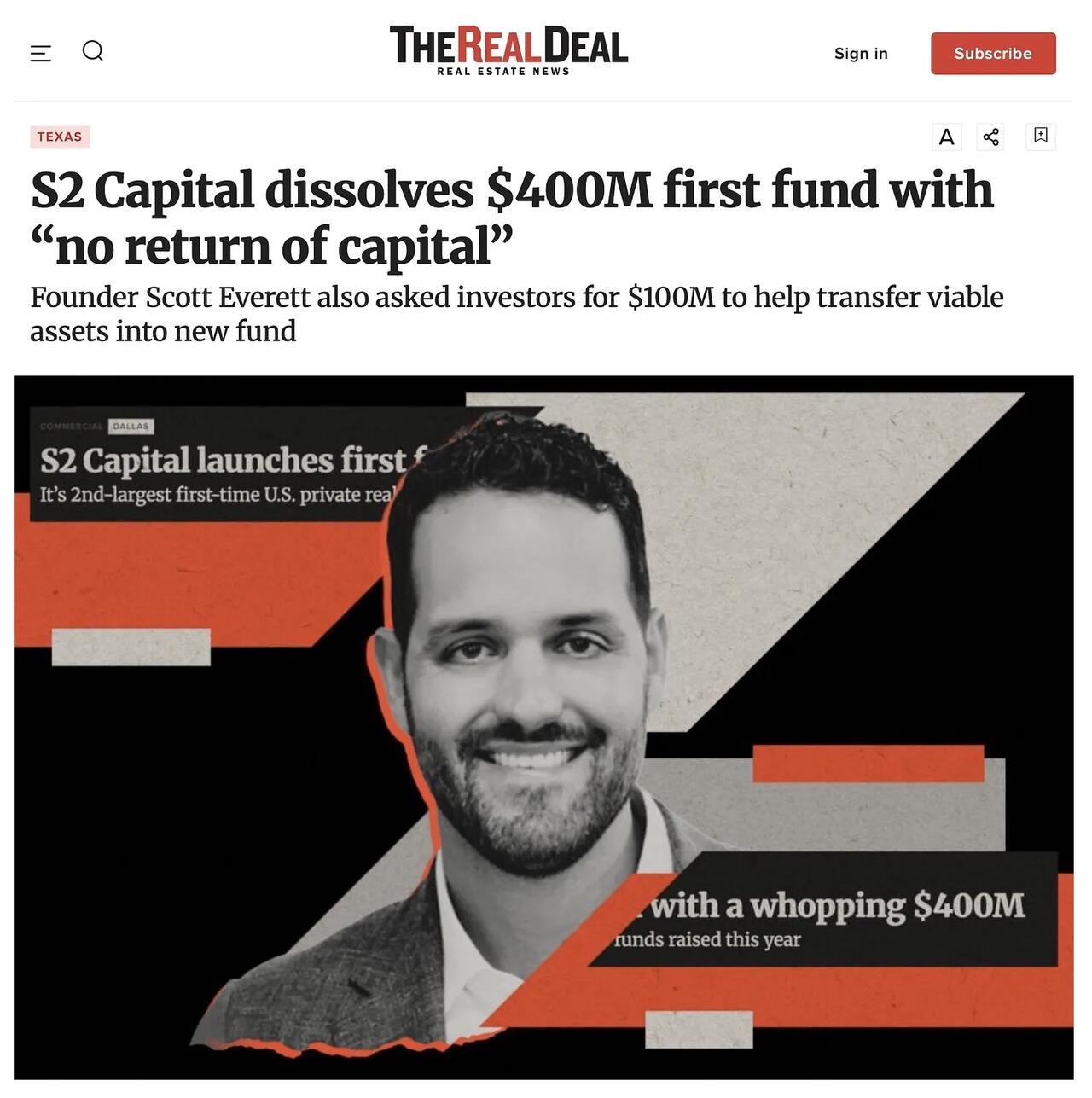

No one gives a f*ck about pointing out over and over things like commercial real estate imploding…until we get a headline like this and a $400 million fund’s capital is completely gone. No capital returned. Total catastrophic loss. And the dickhead running the fund is asking for another $100 million. Go figure.

So how should I expect people whose entire investing life has existed inside this environment to react when I argue that executives should actually be held accountable for their words? Exactly the way many of them are reacting now. Fear. FUD. “Hater.” “Doomer.” Meanwhile I’m watching people whose intellect I genuinely respect bend themselves into pretzels defending executives worth hundreds of millions of dollars because questioning management has somehow become taboo.

Think about how bizarre that really is. Public companies are not monarchies. CEOs are not kings. Being publicly traded is a privilege. Having access to essentially unlimited public capital through equity markets is an extraordinary privilege. Being included in major indexes that generate automatic buying regardless of valuation is an extraordinary privilege. Executives don’t own that privilege. Shareholders do. CEOs work for shareholders, not the other way around. They owe shareholders honesty. They owe shareholders consistency. They owe shareholders credibility. They owe shareholders decisions made in the owners’ best interests, not whatever best protects management’s compensation, reputation, or personal wealth.

If an executive repeatedly tells investors one metric defines success and then quietly stops talking about it once the trend reverses, investors should ask why. If an executive changes the story after raising billions based on the previous story, investors should ask why. If accounting appears aggressive, investors should ask why. If incentives appear misaligned, investors should ask why. None of that is negativity. That’s literally what investing is supposed to look like. Somewhere along the way we’ve convinced ourselves that accountability is bearish. It isn’t. It’s adulthood. Grow the f*ck up.

The uncomfortable reality is that more than twenty years of extraordinary monetary policy have conditioned markets to reward almost everything: unprofitable companies, financial engineering, sky high multiples, questionable capital allocation, narrative over cash flow, momentum over fundamentals. The passive bid buys regardless. Options dealers hedge regardless. Liquidity flows regardless. Every time prices wobble, investors instinctively expect another rescue. That environment doesn’t simply distort asset prices. It distorts judgment itself.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

People lose the ability to distinguish between genuine business quality and abundant liquidity because abundant liquidity has made almost everything look like genius. When every tide lifts every boat, everyone suddenly thinks they’re an exceptional sailor. Eventually skepticism itself begins looking irrational because the market has become completely uncalibrated from reality. If prices no longer reflect economic fundamentals, then the people participating in those markets slowly lose their own calibration as well. Their judgment becomes distorted because the measuring stick itself has become distorted. When the market stops rewarding discipline and starts rewarding whatever can attract liquidity, eventually investors stop recognizing the difference.

Which brings me back to why people call me a doomer. I’m not. I’m a skeptic. It only looks like doom because the reference point has become so detached from economic reality that merely insisting on truth sounds pessimistic. If you’ve been force fed unlimited liquidity, meme speculation, gamma squeezes, passive inflows, monetary expansion, and asset inflation for most of your investing life, someone saying, “Hold on. Does offering a 12% dividend when junk bonds trade at 6% and your company has no cash flow actually make some kind of sense?” sounds like they’re predicting the apocalypse. They’re not. They’re simply asking whether reality still exists.

I don’t blame anyone for pushing back. In fact, I’m glad. If my criticism makes people uncomfortable, good. Discomfort usually means we’ve found an assumption that hasn’t been examined closely enough. Rather than assuming I’m motivated by fear or negativity, I would encourage people to examine their own investment thesis instead.

Ask yourself why basic skepticism feels so threatening. Ask yourself why demanding honesty from executives feels controversial. Ask yourself why questioning valuation feels offensive. Ask yourself why accountability sounds like pessimism.

Those are much more interesting questions than whether I’m a doomer because I don’t think I am. I think I’m standing in roughly the same place I’ve always stood. The difference is that today’s market has drifted so far into euphoria that ordinary skepticism now looks like radical pessimism. I’m not living in a darker reality than everyone else. I’m simply refusing to wear the rose colored glasses that so many investors have slowly mistaken for reality the last 2 decades — and even that assumption I’ve tried to challenge honestly.

Now if you’ll excuse me, I’m going outside to touch grass…

--

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions.

As of May 20, 2026 I personally no longer actively trade (read my story here). My investing/saving is done by recurring contributions mostly to sector ETFs and a few select equities, trusted third parties who oversee my accounts, and advisors. Such advisors or funds, through individual equities, options, index funds, mutual funds, ETFs, or other securities, may have positions in, exposure to, or holdings of names mentioned herein that I know nothing about. Basically, via index funds, ETFs and individual equities it is possible I could own, have exposure to, or not own anything at any point. As of the same date, May 20, 2026, in an attempt to lead a healthier lifestyle, I’ve also excluded myself from fantasy sports, sports betting, online and in-person casinos and prediction markets.

And all positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Related Markets

All MarketsMarket data may be delayed. Not financial advice.

💡 AI analysis provides alternative perspectives on current events

{kind=link}

{kind=link}

{kind=link}

{kind=link}